Hiring help to prompt a series of federal, state and local requirements with regard to wages, verifying the eligibility of employment, reporting of new hires, withholding taxes, social security taxes, Medicare taxes, unemployment insurance, workers compensation, disability insurance, and reporting responsibilities.

It is very unlikely that any persons assisting or acting as the provider’s substitutes are an independent contractor so he/she will need to take caution.

Many employers misclassify staff mistakenly or misclassify staff in order to reduce taxes, insurance costs, and record-keeping responsibilities. Yet, this can be a costly error.

Due to the complexities of a provider’s responsibilities as an employer, he/she may want to consider using a payroll service, which will perform the accounting, payments, and reporting. Some banks offer the service with their business accounts.

In an effort to ensure a healthy and safe environment for children in childcare, THe New York State Office of Children and Family Services (OCFS) developed regulations limiting the number of children in attendance per adult present. OCFS mandates one caregiver for every two children in attendance under the age of two years.

The regulations regarding the child to staff ratios and infant to staff ratios may mandate that a family child care provider has an assistant.

This person would most appropriately be classified as an employee, regardless of the number of hours worked or amount compensated. See “Can I Classify Assistants or Substitutes as Independent Contractors?”

There is a host of responsibilities as an employer. A provider may want to consider using a payroll service or opening a small business checking account with payroll service to assist with the complexities of calculating, reporting withholding and payroll taxes.

Responsibilities as an Employer

Verify work eligibility – The employer must verify the identity and employment authorization of individuals hired for employment in the United States. All U.S. employers must ensure proper completion of Employment Eligibility Verification (Form I-9). The I-9 is not filed with United State Citizenship and Immigration Services (USCIS) or U.S. Immigration and Customs Enforcement (ICE). The form must be retained and stored by the employer for up to for three years after the date of hire or for one year after employment is terminated, whichever is later. The form must be available for inspection by authorized U.S. Government officials from the Department of Homeland Security, Department of Labor, or Department of Justice.

Persons authorized to work in the United States are:

- Citizens of the United States

- Non-citizen nationals of the United States

- Lawful permanent residents, and

- Individuals with the authorization to work in the U.S.

Reporting New Employees/Hires

A childcare provider must report newly hired or rehired employees who will be employed in New York State within 20 calendar days from the hiring date. He/she cannot submit a report without an employee’s Social Security Number (SSN).

This can be done online at www.nynewhire.com or; via mail by sending a copy of the employee’s Employee’s Withholding Allowance Certificate (Form W-4) or Employee’s Withholding Allowance Certificate (Form IT-2104) – to:

New York State Dept of Taxation and Finance

New Hire Notification

PO Box 15119

Albany NY 12212-5119

Or

By faxing the above form(s) to (518) 320-1080.

The W-4 is used as a basis for calculating of the correct withholding of federal income tax from an employee’s pay.

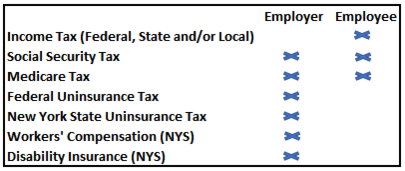

Tax Responsibilities

Some taxes are paid by both the employer and employee, while others are paid solely by the employer or the employee.

Withholding (Income) Tax

Although the withholding tax is paid solely by the employee, it is up to the employer to calculate the correct amount to be withheld and for transfer funds and make payments. Please see below for instructions on how to make payments.

There are several ways to figure income tax withholding (Wage Bracket Method, Percentage Method, or Alternative Methods.) Each requires the employee’s W-4 and use of tables in Publication 15 (Circular E), Employer’s Tax Guide.

Social Security

Both the employer and the employee pay 6.2% of wages toward Social Security. The Social Security Wage Base (SSWB) limit (the amount of wages submect to taxes in a gien time period) is $118,500, beyond this amount both employer and employee need not collect Social Security tax. The information provided on Form W-4 does not change the amount of Social Security taxes.

Medicare Tax

Medicare tax is 1.45% each for the employer and the employee. There is no wage limit for Medicare taxes so all wages are subject to withholding. The information provided on Form W-4 does not change the amount of Social Security taxes.

FUTA Tax

The Federal Unemployment Tax Act (FUTA), with state unemployment systems, provides for payments of unemployment compensation to workers who have lost their jobs. Most employers pay both a federal and a state unemployment tax. Employees do not pay federal unemployment taxes.

The FUTA tax is 6.2% on the first $7,000 paid to each employee during a calendar year after subtracting any payments exempt from FUTA tax.

The wages for the services of an individual who works for his or her spouse in a trade or business are subject to income tax withholding, social security and Medicare taxes, but not to FUTA tax.

Payment for the services of a child under age 21 who works for his or her parents, whether or not in a trade or business, are not subject to FUTA.

Payments made to a parent employed by his or her child are not subject to FUTA tax, regardless of the type of services provided. The employer is the first subject to the state tax. Then the tax becomes a credit against federal tax.

Note: Payroll taxes (social security, Medicare, federal unemployment tax, and state unemployment tax) are deductible business expenses. Learn more about taxes here.

Reporting Responsibilities

Federal Form 941

The Employer’s Quarterly Federal Tax Return (Form 941) quarterly withhold income taxes, social security tax, or Medicare tax from employee’s paychecks. THe form is due on the following dates: April 30, July 31, October 31, and January 31.

Report the following amounts.

- Wages paid by the provider;

- Tips employees have received;

- Federal income tax withheld by the provider;

- Both the employer’s and the employee’s share of social security and Medicare taxes;

- Additional Medicare Tax withheld from employees;

- Current quarter’s adjustments to social security; and

- Medicare taxes for fractions of cents, sick pay, tips, and group-term life insurance.

Federal Form 940

The due date for filing Form 940 for 2016 is January 3, 2017. However, if a provider deposited all FUTA tax when it was due, he/she may file Form 940 by February 10, 2017.

Federal Form 944

Form 944 is for employers whose annual liability for social security, Medicare, and withheld federal income taxes is $1,000 or less for the year.

Form NYS-45

Employers in New York State must electronically submit a Quarterly Combined Withholding, Wage Reporting and Unemployment Insurance Return (Form NYS-45). File the NYS-45 online. For more information, call (888) 899-8810.

W-2

Employers must issue W-2s to employees by Jan. 31. The W-2 shows the amount of compensation paid to employees and the amount of tax withheld for the year. The data is used by Social Security to update an employee’s lifelong earning history and then, from that earning history, calculate the employee’s benefits. An employer can be assessed a penalty for W-2 names and Social Security numbers that do not match.

An employer can use W-2 Online to complete W-2 forms and print copies suitable for distribution to employees. In order to do this, the employer must register at https://secure.ssa.gov/acu/IRESWeb/registration.jsp

Making Payments of Withholdings and Payroll Taxes

Generally, federal payments are made via electronic fund transfers by using the Electronic Federal Tax Payment System (EFTPS). For more information visit EFTPS.

There are two situations where you might hire someone to help you care for children and the person would be considered an independent contractor.

The first situation is a person who is self-employed in the business of providing substitute care for child care providers. Such a person should have a business name registered with your state and their own taxpayer identification number. She/he should work for more than one child care provider each year and use his/her own contract.

The second situation is when you hire a substitute through an employment agency and you pay the agency rather than the substitute.”

It is a mistake that could prove to be very costly to the business owner, who may end up owing employee-related costs like back taxes and any applicable penalties for state and federal income taxes.

Resources and links:

- http://tomcopelandblog.com/are-your-helpers-employees-or-independent-contractors

- https://www.irs.gov/publications/p15a/

- https://www.irs.gov/taxtopics/tc762.html

- http://www.wcb.ny.gov/content/main/Employers/Coverage_wc/emp_empDefinition.jsp

- http://www.ncsl.org/research/labor-and-employment/employee-misclassification-resources.aspx

When purchasing workers’ compensation insurance, an employer is buying the following protections:

- Medical services needed to treat the job injury or illness;

- Temporary disability payments to the employee to help replace lost wages;

- Permanent disability payments to the employee to compensate for permanent effects of the injury;

- A death benefit for the employee’s survivors in the event of a fatal injury;

- Legal representation for the employer by the insurance carrier;

- Protection for the employer against most lawsuits for on-the-job injuries/illnesses.

The employer must pay for the cost of insurance coverage, as it illegal to require employees to pay any of the costs associated with workers’ compensation premiums or injuries.

Family members providing paid or unpaid services to a for-profit business are counted as employees for workers’ compensation coverage purposes.

The New York State Workers Compensation Board has the legal authority to require employers to provide coverage and can penalize those who do not. Furthermore, New York State Office of Children & Family Services (NYSOCFS) requires that family childcare providers obtain workers’ compensation before putting employees to work and submit documents verifying this coverage. Learn more about regulations –here.

An employer’s failure to provide workers’ compensation coverage is a crime, punishable by fines and/or criminal prosecution. A stop work order may be issued. Add onto that the legal cost of defending and possibly losing a civil suit for an injury of an employee, and the cost of workers’ compensation insurance is very reasonable.

The New York State Disability Benefits Law is part of the New York State Workers’ Compensation Law. If a provider employs one or more employees for 30 days in any calendar year, then he/she must obtain disability benefit insurance.

How to Obtain Coverage

A childcare provider can obtain coverage through:

Workers’ Compensation

State Insurance Fund (a public insurance carrier in New York State)

NYS Insurance Fund

http://ww3.nysif.com/

1-888-875-5790

A provider can also find coverage through the more than 200 private insurance carriers authorized by the New York State Insurance Department to provide workers’ compensation insurance to employers. If appropriate, look through The Real Yellow Pages (yp.com), contact an insurance broker, carrier or agent, check with a trade association, or conduct additional research to find the most appropriate insurance coverage for the company.

Disability Insurance

NYS Insurance Fund

http://ww3.nysif.com/

1-888-875-5790

Both Workers’ Compensation and Disability Insurance premiums are tax-deductible business expenses. Find more information about taxes here.

Employers must post a Form Notice of Compliance – Workers’ Compensation Law (C-105).

Resources and links:

Click to play video in new window:

http://www.bronxnet.org/tv/viewvideo/4888/open–legal-corner-with-david-lesch/workers-compensation

There are many insurance companies, so selecting one can be a challenge. Here are the main points to keep in mind when selecting an insurance company that’s best for the business.

Licensing

Not every company is licensed to operate in each state. As a general rule, a provider should buy from a company licensed in his/her state. THis way, should a problem arise he’she can contact the state insurance department for help. To find out which companies are licensed in your state, contact the state insurance department.

Price

Many companies that sell insurance policies have prices that vary greatly from one policy to another, so it really pays to shop around. It is recommended that a provider obtain at least three price quotes from companies, agents, and the Internet. Your state insurance department may publish a guide that shows what insurers charge for different policies in various parts of your state.

Financial Solidity

A provider should buy insurance for financial protection and peace of mind. Select a company that has a track record of being financially sound. Learn more about the company by using ratings from independent rating agencies.

Service

An insurance company and its representatives should answer questions and handle claims fairly, efficiently and quickly. Get a feel for a company by talking to other customers who have used its services or have been serviced by its agent(s). Also, check a national claims database to see what complaint information, if any, it may have on the company. In addition, the state insurance department can provide information about whether an insurance company has consumer complaints about its service relative to the number of policies sold.

Comfort

A childcare provider should feel comfortable with his/her insurance purchase, whether brought from a local agent, directly from the company over the phone, or over the Internet. Make sure the agent or company will be easy to reach if there are any questions or a need to file a claim.

New York workers’ compensation loss rates vary by industry class codes and insurance company underwriting standards. Every insurance carrier must utilize these manual rates to develop premium.

As of Oct. 1, 2016, the loss rate for class code 8869 CHILD DAY CARE CENTER PROFESSIONAL EMPLOYEES AND CLERICAL, SALESPERSONS was $1.59 per employee per day. Note this is not necessarily the premium rate.

Resources and Links:

Anyone hired by the childcare provider must be treated as an employee regardless of whether or not the individual is a family member. As the employer, the provider owes federal unemployment taxes even if the family member is his/her own child who is 18years or older and earns less than $600 a year. The employer is responsible for withholding income tax, payment of social security tax, Medicare tax, and unemployment insurance tax. For more information see Responsibilities as an Employer.

If the provider hires his/her own child who is under the age of 18, then he/she is not required to pay Social Security/Medicare taxes, state or federal tax and the child can earn up to $5,700. Hiring family can provide unique benefits in that the provider can deduct the wages paid and his/her child probably won’t have to pay any taxes.

In New York state family members providing paid or unpaid services to a for-profit business are counted as employees for workers’ compensation coverage purposes.

Resources and links:

- http://tomcopelandblog.com/to-hire-a-relative-or-not

- http://www.wcb.ny.gov/content/main/Employers/EmployerHandbook.pdf

- http://www.irsvideos.gov/SmallBusinessTaxpayer/Employers/EmployingFamilyMembers

For additional information about hiring family see – Publication 15 (2015), (Circular E), Employer’s Tax Guide and Publication 15-A (2015), Employer’s Supplemental Tax Guide.

As a family childcare business owner, it is highly unlikely that you would be required to provide health insurance to your employees. According to the federal site, healthcare.gov you don’t have to offer health coverage “if you have 1-50 (full-time equivalent FTE) employees. You can choose to offer insurance through the Small Business Health Options Program (SHOP) Marketplace or any other source. But you don’t have to, and you don’t face a penalty if you don’t.”

Should a provider opt to provide health insurance, healthcare.gov states that he/she may qualify for the Small Business Health Care Tax Credit.

It is not required that a provider offer coverage to part-time employees (those working fewer than 30 hours per week), or to dependents in order to qualify for the tax credit.

As an employer, a provider will have to follow a host of state and federal laws that regulate his/her relationship with employees. It is important that the provider become familiar with these since non-compliance can lead to penalties and/or criminal charges.

The New York State Office of Children and Family Services in its Family Day Care Provider Handbook suggest that you review federal and state employment laws whenever you add new employees.”

Source:

http://www.nolo.com/legal-encyclopedia/workplace-employment-laws-employer-29957.html

The minimum wage varies from state-to-state, and even between local city government. Workers are entitled to whichever is highest: the federal, state, or local minimum wage. The state minimum wage rate is generally applicable to all employees who are non-tipped individuals and perform work in New York State.

A provider can visit the U.S. Department of Labor Minimum Wage Map to learn more about New York State’s minimum wage rate.

New York State labor law requires employers to post the provisions of the Minimum Wage Act; poster here.

Resources and Links: